Russia has more than doubled its interest rate to 20% in a bid to halt a slump in the value of its currency.

The Bank of Russia raised the rate from 9.5% after the rouble sank 30% after new Western sanctions. The currency then eased back to stand 20% down.

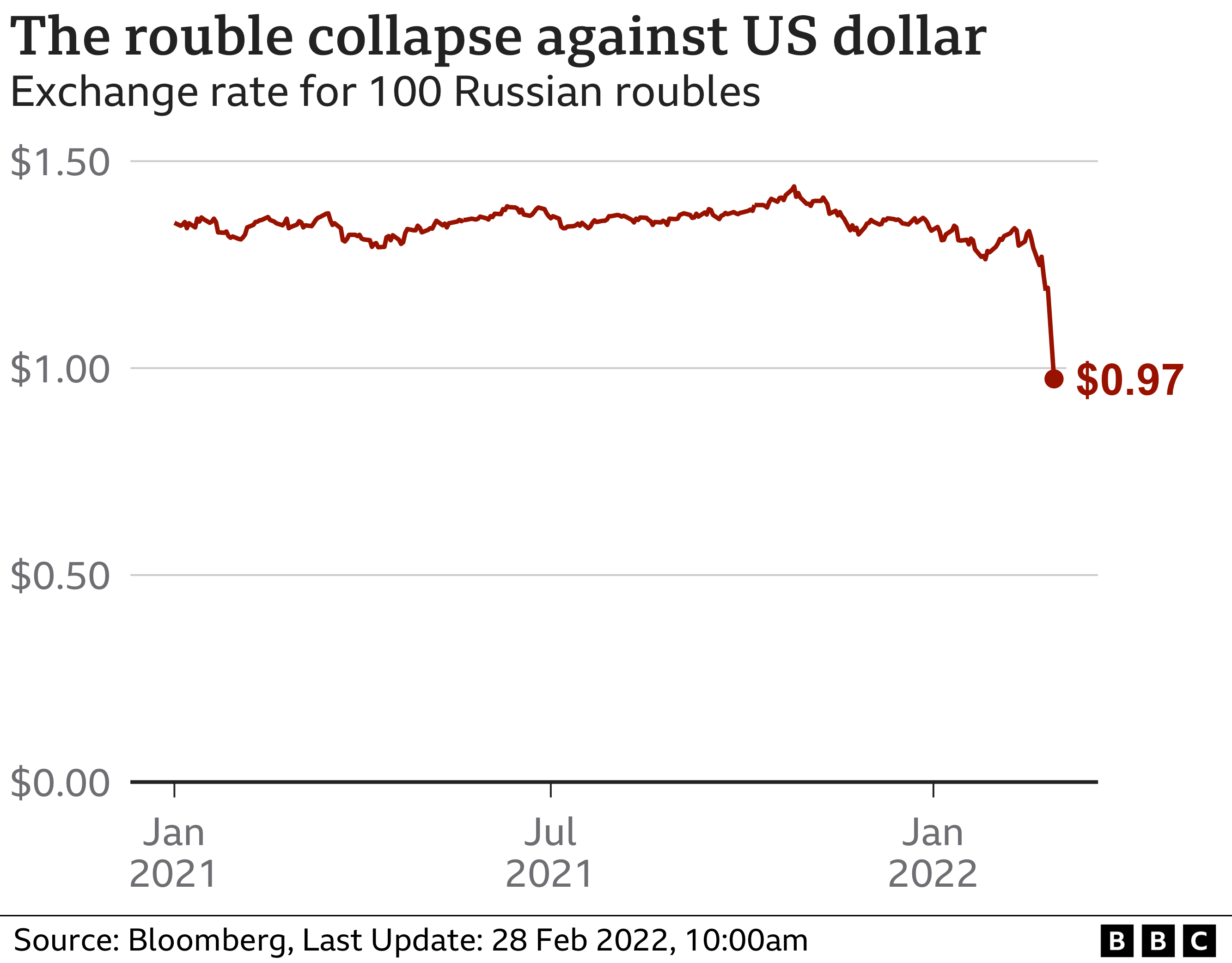

The collapse in value erodes the currency's buying power and could wipe out the savings of ordinary Russians.

Amid pictures at the weekend of queues at cash machines, Russia said it had the resources to ride out sanctions.

Ahead of an emergency meeting between President Vladimir Putin and his economic advisers on Monday, Kremlin spokesman Dmitry Peskov said: "These are heavy sanctions, they're problematic, but Russia has the necessary potential to compensate the damage from these sanctions." He said Russia would respond with its own sanctions.

At the weekend, Russia's central bank issued an appeal for calm amid fears that new financial sanctions could spark a run on its banks. It said it had the "the necessary resources and tools to maintain financial stability."

Videos on social media appeared to show long queues forming at cash machines and money exchanges in Moscow, with people worried that their bank cards may stop working or that limits will be placed on the amount of cash they can withdraw.

It came as the UK, along with the US and EU, cut off Russia's banks from financial markets in the West, prohibiting dealings with the central bank, state-owned investment funds and the finance ministry.

Chancellor Rishi Sunak said the measures demonstrated the UK's "determination to apply severe economic sanctions in response to Russia's invasion of Ukraine".

Russia has about $630bn (£470bn) in reserves - a stockpile of savings - built up from soaring oil and gas prices.

But because a lot of this money is stored in foreign currencies like the dollar, the euro and sterling as well as gold, a Western ban on dealing with Russia's central bank restricts Moscow from access to the cash.

Last week, Russia's central bank was forced to increase the amount of money it supplies to ATMs after demand for cash reached the highest level since March 2020.

On Monday, the central bank said it had ordered brokers to suspend the execution of all orders by foreign legal entities and individuals to sell Russian investments.

It also said it had yet to decide whether to open markets other than foreign exchange and money markets on Monday.

The sanctions that have been imposed by the EU, the US, the UK and others are unprecedented. It's one thing to block the foreign reserves of a country like Iran or Venezuela, quite another to act against Russia - a country with a major role in global trade and a very significant supplier of oil and gas.

The reaction on the currency markets has been dramatic - with the rouble plummeting, despite the central bank's efforts to prop it up using interest rates. There may already have been a rush to the foreign currency ATMs in Russian cities, but citizens there have yet to feel the full impact.

At the very least prices will rise dramatically; banking collapses, hyperinflation and a deep recession are all potential consequences.

But sanctions are a two-way street. Cutting the central bank off from its reserves and limiting Russian institutions' access to the Swift network will not only hurt Russia - western institutions also face losses from debts that cannot or will not be repaid, for example. And then there is the risk of countermeasures from Russia - potentially hitting energy exports.

Such sweeping sanctions being imposed in such a unified way is remarkable. It's also a very big gamble.

'Economic pariah'

Attempts to put a stranglehold around Russia's finances is sending shockwaves across the financial and corporate world, including:

- The price of gas for delivery over the next couple of months soared by 24%

- European markets fell amid fears over financial stability, with London's FTSE 100 down more than 1% and Paris and Frankfurt about 2% lower

- The price of crude oil jumped 5.4% to $103 per barrel, and the dollar and gold rose as investors sought safer places to put their money

- BP's share price slumped by 7% after it decided to exit Russian oil and gas operations at a cost of up to $25bn

- Equinor, the energy firm majority owned by the Norway government, starts to divesting its joint ventures in Russia

- Wheat prices see their biggest one-day gain in a decade on supply worries from Russia and Ukraine

- Russia's stock market remains closed amid fears of a massive share sell-off

Will Walker-Arnott, senior investment manager at Charles Stanley, told the BBC's Today programme that "it looks like Russia is increasingly becoming an economic pariah, increasingly isolated from the global financial system".

Cutting some Russian banks from international payments system Swift is the harshest measure so far imposed to date on Moscow over the Ukraine conflict.

The assets of Russia's central bank will also be frozen, limiting the country's ability to access its overseas reserves.

Russia is heavily reliant on the Swift system for its key oil and gas exports.

The intention is to "further isolate Russia from the international financial system", a joint statement said.

On Monday, the European Central Bank (ECB) said several European subsidiaries of Sberbank Russia, which is Russia's largest bank and majority owned by the Russian government, were failing or likely to fail due to reputational cost of the war in Ukraine.

Sberbank Europe AG, which had total assets of €13.64bn (£11.4bn) at the end of last year, along with its Croatian and Slovenian units, suffered a rapid deposit outflow in recent days and is likely to fail to pay its debts or other liabilities, said the ECB, which is the lenders' supervisor.

0 Comments